TROUTWOOD

Designing Wealth

Company

Role

Product Designer

Researcher

Team

UX Researchers

Product Designers

About Troutwood

Troutwood is a SaaS, conflict-free financial planning platform with a B2B2C business model. Recognizing that individuals of all financial literacy backgrounds would benefit from having a financial plan, Troutwood aims to make financial planning accessible to all, especially those who are underprivileged.

“Financial self-efficacy is strengthened by self-esteem, and high financial self-efficacy leads to positive financial attitude and behavior.”

— Noh & Mijeong (2022)

The Challenge

INSIGHT 1

Money is Emotional

We learned that emotions can be both a barrier and a catalyst to changing financial behavior. For some, managing money is empowering and invigorating. For others, negative mental models about money, fear, distrust, and shame act as barriers to taking action on their financial situation.

INSIGHT 2

Information Overload Deters Action

Financial concepts can be abstract and difficult to grasp, and the overuse of technical jargon further complicates learning. This can lead to cognitive overload and information overload as users struggle to process and make sense of the information presented to them.

INSIGHT 3

Financial Goals are Too Distant to Imagine Concretely

Even when individuals rationally understand that they should start saving and investing early to kickstart their financial journey, the vast majority of people cannot accomplish this. People are often overwhelmed with the pressing financial needs they have in front of them, allowing longer-term goals to fall to the bottom of their hierarchy of needs.

Research

Background Research

-

17 Product Walkthroughs

of Troutwood, its competitors, and analogous domains

-

5 Expert Interviews

of finance industry professionals and one Psychology expert

-

38 Interviews

to learn about financial behaviors and attitudes

-

31 Literature Reviews

of published papers on financial literacy, financial empowerment, and behavior change

Findings

When it comes to financial matters, participants experience a Psychological phenomenon known as learned helplessness – a self-reinforcing cycle of stress that leads to avoidance of their financial situation. This can look like postponing opening a savings account, not taking steps to improve their finances, or avoiding increasing their financial literacy. Learned helplessness is a lose-lose situation as it not only leads to poorer financial outcomes but can also lead to lower self-esteem.

Additionally, the financial education space is highly saturated with advice from many sources. This information overload makes it impossible to start sifting through the wealth of information, including websites, social media influencers, financial advisors, or even malicious scammers. For an individual with low financial literacy, a lack of generational knowledge, and an inability to hire a trustworthy financial advisor, distrust is highly prevalent.

On top of all of this, those with the fewest resources are often the most vulnerable to financial threats such as scammers and get-rich-quick schemes. Those who grew up with generational knowledge are much more likely to be able to make wise financial decisions and start saving and investing early, which sets them up for later success.

“There is a sense of gatekeeping... It feels like I can't ever learn the rules.”

— Participant

“Financial literacy is the most important factor that plays a critical role in making the financial decisions, especially in making the future plans, financial issues, money matters discussion, and responding to financial threats of life.”

— James, Cobanoglu & Cavusoglu (2021)

Finally, a major hindrance to achieving financial wellbeing is the difficulty of carrying through on distant goals. Even highly motivated individuals who have worked hard to learn about finance find it difficult to prioritize non-immediate goals, such as saving for retirement or a down payment for a house. Research finds that people choose to deprioritize distant goals in favor of more immediate forms of gratification.

“The more distant a goal is, the more difficult it is for people to imagine it concretely.”

— Bucher, Engaged (2020)

Generative Research

-

Usability Tests

of the flagship Troutwood app

-

Semi-Structured Interviews

of target users to learn about their attitudes and financial habits

-

Directed Storytelling

of participants’ previous experiences with saving, spending, and investing

-

Artifact Analysis Activity

where participants created their own financial dashboard

Findings

Throughout our research, we recognized that financial planning is highly subjective to an individual’s situation and attitudes. Certain tools may be helpful for some but irrelevant for others, like how sophisticated stock market data would be overwhelming for a beginner. To honor this and ensure only relevant and helpful information is shown, our team synthesized qualitative data from semi-structured interviews to identify the key jobs-to-be-done our users have. The four biggest jobs-to-be-done were debt management, savings building, financial education, and goal-setting.

When speaking with users, we began to realize that many of them had the means to begin saving and financial planning, and even recognized the importance of it, yet did not take concrete steps to do so. We realized that a big piece of the puzzle we had previously been missing was the importance of behavior design principles in encouraging habit formation. Some users reported initiating positive financial behaviors, such as opening an investment account or starting a budget, yet only a small percentage followed through on these behaviors regularly. Incorporating behavior design principles such as reinforcement learning, cognitive load balancing, and soft incentives into the product encourages users to have more positive financial behaviors as well as follow through on the financial plans they create.

“I'll go through phases when I’m really vigilant about my money… I’ll start a budget that’s really good but then two weeks later I stop following it and never actually meet my savings goals.”

— Participant

“I know that I should have a budget, and be saving up for big stuff like an emergency fund or something, but it just feels so impossible when I have so much other stuff I need to focus on at all times like just paying the bills or my loans.”

— Participant

Recruiting and sorting our participants based on their job-to-be-done, we conducted an artifact analysis activity where we asked participants to build their own financial dashboard. We got to learn about users’ financial priorities and what features need to be front and center, such as an at-a-glance budget, recent transactions, or student loan information. This helped us to begin ideating how our app should populate based on user data collected during onboarding.

“A lot of what I want [on my dashboard] is based on my current needs. Like I’m really stressed about my student loans, so I want to be able to keep a close eye on that right now".”

— Participant

Ideation

Based on the financial priorities identified in our artifact analysis activity and recognizing how many features the product would need to have, our team created an information architecture. We were intentional to make sure we had both a breadth and depth of fidelity, as we would run the risk of alienating potential users if a key feature needed in the financial planning process was missing. The information architecture helped us to identify the key flows to build:

Onboarding

The dashboard

Creating a long-term financial plan

Setting short-term goals

Debt management

Research shows that overly restrictive budgeting has adverse effects on mental health, so we never wanted our users to feel that they had to cut out all their smaller joys in life to meet their long-term goals. Our team initially struggled to figure out how a short-term goal, like saving up for a vacation, should factor into long-term goals, like saving for retirement, in terms of the user’s interaction with the app and the backend computation.

Additionally, most existing financial apps focus only on the short-term – like budgeting apps that help users spend within their earnings every month – but do not take into account longer-term goals. This is problematic as users may end up overspending if they do not have long-term goals in sight. Therefore, we decided that Troutwood needs to encourage the user to express all goals, both long- and short-term, and make suggestions for budgetary adjustments accordingly.

Take, for example, a user’s long-term goal of saving one million dollars for retirement — a goal that Troutwood says will take 18 years based on her current earnings and spending habits. The user initiates a new goal, a vacation to Europe, that she hopes to achieve within a year. Since the app’s budget is currently maximized to help the user reach her retirement goal and does not account for a European vacation, adjustments need to be made so she can stay on track for both goals. It can be disheartening and cause users to give up if they only see that their short-term desires are a hindrance to their long-term goals, rather than realize they can coexist. To combat this, Troutwood should make suggestions to the user that ultimately empower her to make the financial decision that is best for her — like:

“you can make both happen if you spend $100 less on eating out each month this year;”

Or:

“if you spend $300 less on the trip you will only need to eat out $70 less per month this year;”

In this scenario, the user chooses a category (or categories) she wants to make adjustments to and decides on what amount works best for her.

How might short-term goals coexist with potentially conflicting long-term goals?

ROADBLOCK

With our key flows identified, we set out to ideate how they might look individually and interact with each other. In onboarding, the app not only has to win over the user and demonstrate its trustworthiness, but also collect important information to determine how the app should populate as users will come from varying levels of financial literacy and needs.

Information conveyed on the dashboard is crucial as it needs to be concise while also prompting users to delve deeper into the app and take important next steps. It should contain a certain level of customizability to account for the differing financial needs of returning users. For first-time users, the dashboard will have prompts that nudge users to finish onboarding steps.

We experimented with collecting necessary information in a guided format, where the user was prompted at every step to provide information such as monthly expenditures, income, and loan information.

Validation Sessions

FINDING

Many users shared they felt intimidated by how “money heavy” our pages were. Relying entirely on numbers to demonstrate progress is visually taxing to read.

We need to find creative ways to show progress in a manner that does not solely rely on numbers. We can use progress bars that visually depict progress, or utilize percentages to show how far the user is from their goal.

FINDING

Users feel the differentiation between a “goal” and a “financial plan” is a bit ambiguous and could be distinguished better.

IMPLICATION

IMPLICATION

We need to make it clear that a goal is a part of the financial plan and that every new goal has a direct impact on other aspects of the plan.

Final Design

Onboarding

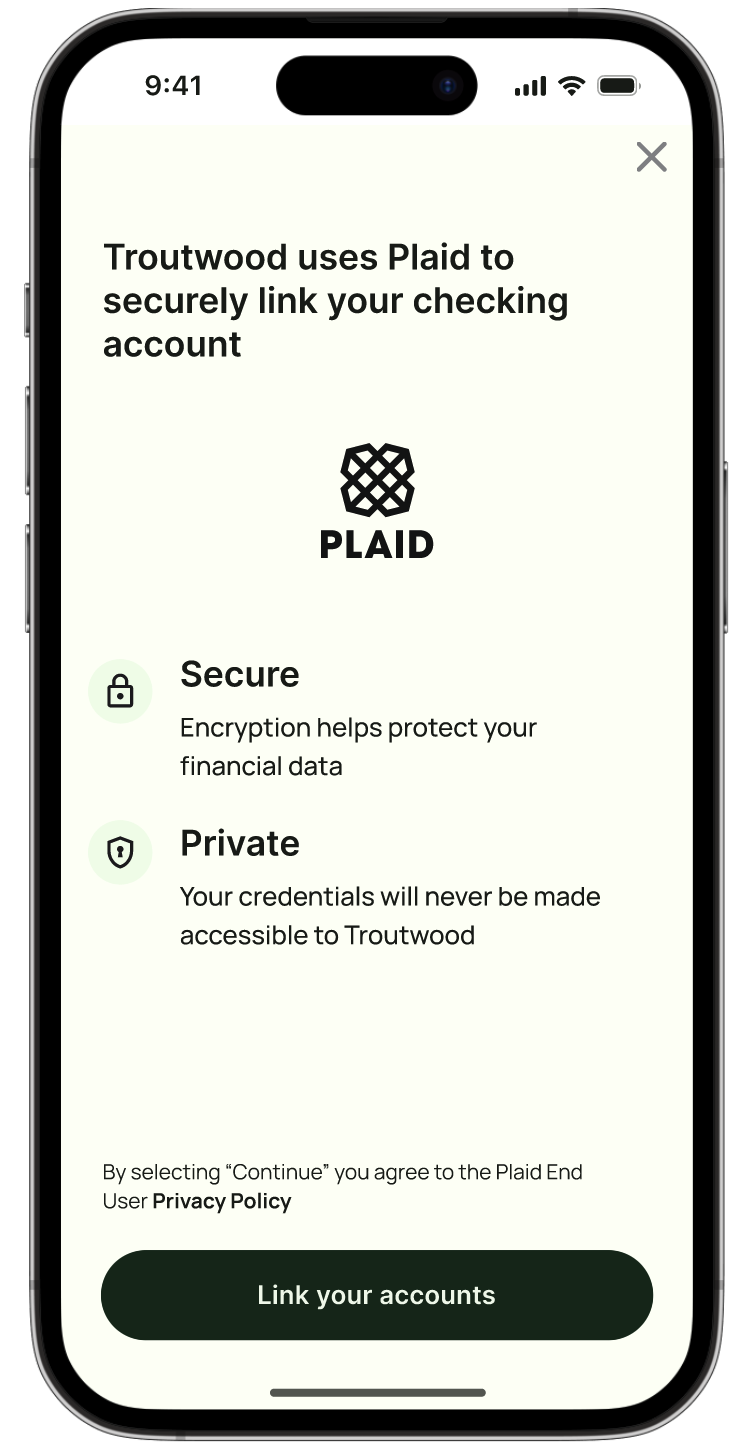

Following user testing sessions on our wireframes, we decided to shorten the onboarding flow in favor of deferred onboarding so as to reduce information overload. We wanted users to have the option to either complete onboarding by linking bank accounts or to enter the home page to get a feel for the app. This was in consideration of the fact that, due to its status as a startup, many users may not have pre-established trust in the brand and may not want to provide sensitive financial information before seeing what Troutwood can offer.

Troutwood utilizes Plaid, the data transfer financial services company, to allow seamless integration of bank information in the app. Plaid gives users the ability to have real-time updates on their financial information, such as account balance and all transactions. Linking accounts is central to almost all of Troutwood’s key features, so it is vital that Troutwood demonstrates value and trustworthiness to the user as soon as possible and encourages them to link their accounts.

Dashboard

The dashboard serves as the central hub that displays important at-a-glance information to the user, with the goal being to demonstrate a breadth of information, rather than depth. Based on which features they utilize, the dashboard will populate with an overall financial wellness check, any loan information, recent transactions, goals, rewards, and financial education materials.

Due to the deferred nature of the app’s onboarding flow, first-time users will see prompts to complete onboarding in place of the cards returning users see. To get the most out of the app, users will not only need to link their accounts to Troutwood via Plaid, but also build a financial plan based on their goals, which includes a budget.

The Financial Plan

The Financial Plan is Troutwood’s rendition of a budget. The name change is because the plan contains much more than just a budget; it comprehensively views all aspects of the financial picture such as debt and financial goals. Users are also given recommended actions based on their progress, such as setting up a emergency fund or starting to set aside money for investments.

Users receive instant feedback on whether or not their expenses for the month have been on track. In this user’s case, even though they have gone above their planned amount in several categories, they are under in others to make up for it. It is crucial that Troutwood comprehensively views the user’s spending as more black-and-white feedback can increase negative affect.

Setting Goals

A crucial interaction between the user and Troutwood’s app is the incorporation of goals, big and small, into the user’s financial plan. Because ideally every expense is accounted for, the user gets a realistic and accurate picture of which goals are feasible. The first part of every goal flow is information gathering, such as the amount of money needed and by when.

Once Troutwood has all the necessary information, it can communicate the feasibility of the goal to the user. The language used here is significant, and must not be discouraging to avoid reintroducing the learned helplessness cycle. Instead, the app should suggest tangible steps that allow the user make the goal a reality.

A crucial aspect of helping users overcome their learned helplessness is the behavioral design principle of Autonomy. Here, the user is given the autonomy to decide which areas of their budget should be adjusted to allow progress toward their goal.

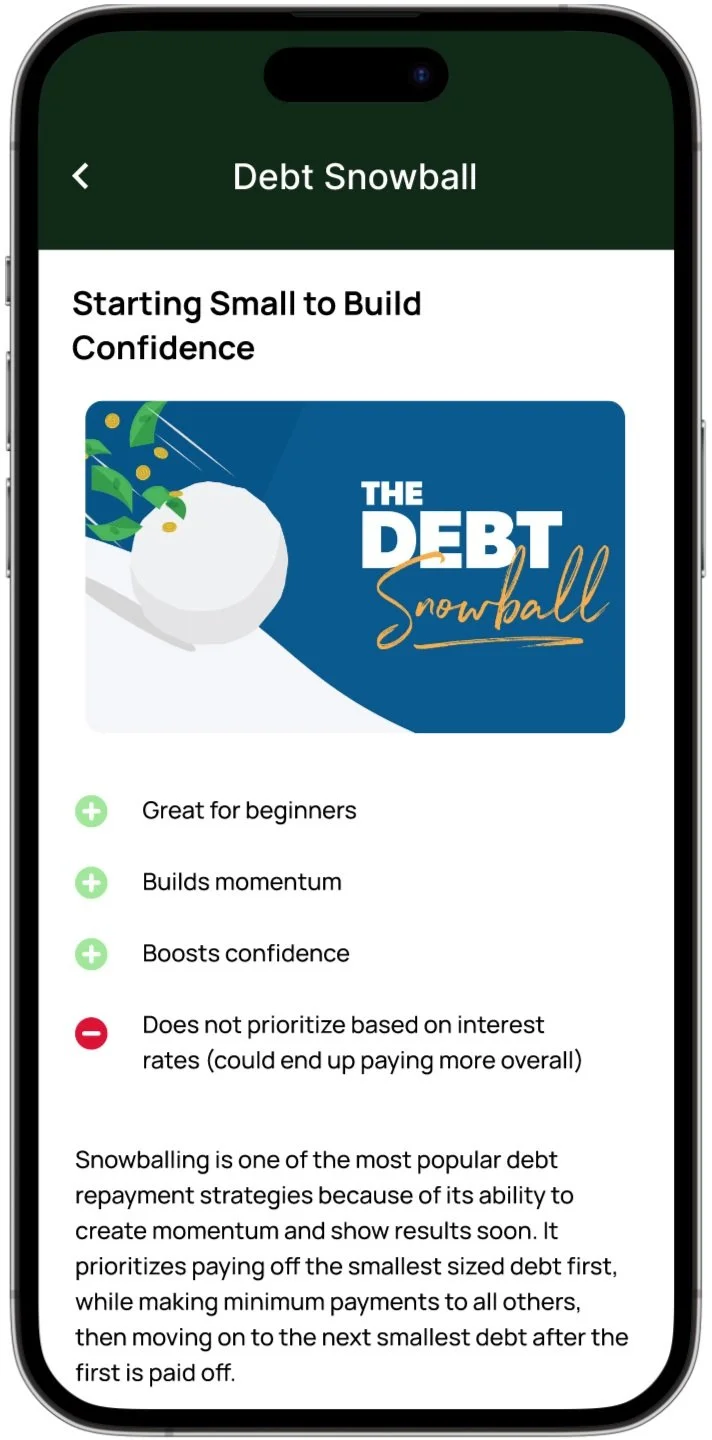

Debt Management

While not necessarily applicable to every use case, debt management is critical given that 77% of Americans are in debt. Debt is a major inhibitor to financial growth, not to mention the significant psychological impacts that come with being in debt. Troutwood gathers all debt information and displays an overview on the main page as well as the user’s debt repayment timeline.

Troutwood recommends proven debt repayment techniques, like the debt snowball, to users to help them set goals for their repayment timeline. Goals that take into account every user’s unique situation allow them to select the strategy that they feel most comfortable with and are therefore more likely to follow.

The debt calculator is a tool within the debt section that allows users to envision a future where they have paid down their debt. They can play around and adjust their monthly payment to see how much in interest and time they would save. This incentivizes users to pay their debt back more aggressively while empowering them to follow a timeline that they feel most comfortable with.

Outcomes

DESIRED OUTCOME 1

Troutwood gains users’ trust and respect in a highly saturated field.

Troutwood communicates their USP and trustworthiness to the user early on by allowing delayed onboarding. Clear and concise UX writing convinces the user that Troutwood is an empathetic and valuable product for those with all levels of financial literacy.

DESIRED OUTCOME 2

Users feel certain about which steps they need to take for the sake of their financial wellbeing.

Troutwood’s nudging, guidance, and powerful backend computations help users determine which goals are feasible and learn how to prioritize their finances.

DESIRED OUTCOME 3

Users overcome learned helplessness, and checking the Troutwood app becomes part of users’ financial habits.

Troutwood supports a user’s financial journey throughout their life, as goals are met and new goals arise. As life circumstances change, salaries shift, and debt gets repaid, the financial plan takes a different shape and users track their progress every step of the way.